The Online Business Tax Playbook (feat. BowTiedTrouserSnake)

Everything you need to know about online business taxes

For today’s article I tagged in @BowTiedTrouserSnake - a tax lawyer with over 15 years’ experience in federal tax law, including the taxation of corporations, LLCs, and partnerships - to give an overview of what you need to know about taxes and your business. You can learn more from TrouserSnake at bowtiedtax.com.

This is an extremely important topic that all online business owners need to think about.

This article represents the personal views of an anonymous cartoon animal. Nothing in the article should be taken as legal, tax, or financial advice. It is a high-level summary of example facts under particular tax laws, and does not go into all applicable exceptions, ancillary rules, and potential case law and IRS rulings. Always talk to your legal, tax, or financial advisor prior to taking any position.

Build internal links to new posts with the click of a button. Speed up your internal linking process and help your articles rank higher in Google with Link Whisper’s intelligent recommendations.

The Online Business Tax Playbook

Tax is likely the biggest expense item on your P&L. If you're not proactively reducing your effective tax rate (reducing taxable income and increasing tax deductions), you're leaving significant money on the table. The IRS isn't going to tell you that you missed a deduction. It's your responsibility to know enough to hold your advisors accountable.

You're running a business. Act like it.

If you’re reading this, you are built differently. You understand that following common knowledge leads to common results - sitting in a cubicle for 45 years until you have enough money to buy a condo in Tampa and die. So you’ve started an online business to escape the cage.

Quit calling it a “side gig” or “side hustle.” It is a business. Act like it.

If you only remember one thing from this article, remember this: if you don’t respect your business, the IRS and the courts won’t respect it either.

Hundreds of tax rulings and court cases have assessed so-called business liabilities against the owners’ personal assets, “piercing the veil” of the corporation or LLC, and throwing out otherwise valid deductions. All because the owners did not respect their businesses enough to treat them seriously.

What do I mean by “respect your business”?

Regardless of the legal/tax form you choose, keep detailed books and records of the business and keep them separate from your personal records. They are the foundation of your defense in the event of an audit.

Get an EIN - the business equivalent of a social security number. They are free to get and usually available the same day on the IRS website. While the IRS does not require one for every business, you will need it to set up the business bank account.

Set up a business bank account. If you have a legal entity, set up the account in the entity’s name. Use this account to receive customer payments and pay all your business expenses.

When you enter into contracts, make sure it is the business (not you) listed on the document. Yes, you’ll often sign the contract, but you are signing “on behalf of” the business.

In any other situation, when there is a choice to do something “as yourself” or “as the business” - use the business.

With that out of the way, let’s get to the sexy tax and legal talk.

Do I Need a Legal Entity?

Ask yourself two questions. First, do I have personal assets of any worth? If you have a home, investment accounts, or material savings, the answer is “yes.” If you live in the backseat of your 1996 Honda Civic, the answer is likely “no.” Certain legal entities limit your personal risk for business liabilities.

Second, what are my current business income and expenses? If the business has expenses in the high four digits or more, it likely benefits from an entity. More deductions will be available and they are less likely to raise eyebrows at the IRS.

An entity is advantageous if you would benefit from liability protection or you have enough business expenses to justify the time and cost of forming and maintaining it.

Which Legal Entity Should I Choose?

Ah, the most common question asked by small business owners. And the hardest to answer in the abstract.

The primary forms used in online businesses are sole proprietorships, partnerships, corporations (“S corps” and “C corps”), and LLCs. Which form you choose impacts the legal and financial complexity and the degree of risk you assume. Therefore, always look at the big picture, including the following:

What is your income and tax situation outside the new business (W-2 income, investment income, etc.)?

Is your net worth large or small?

Do you have co-owners?

What revenue and expenses does the business currently generate?

Do you expect that to grow significantly?

Do you have employees or do you plan to hire any?

Is your goal to sell the business down the road?

Your answers to these questions will help you make a better decision about which entity you choose. HOWEVER, do not fall victim to analysis paralysis. There are a million articles you could read arguing about which entity is “best.” Understand the basics, form your entity, and get back to running your business. Few entity choices can’t be changed later with a decent tax advisor.

Get access to full-length SEO guides, Q&A sessions, and premium business content not found anywhere else. Become a paid subscriber today.

Overview of Legal Entity Types

Sole Proprietorships (i.e., “no entity”)

Advantages: Simplicity and cost. Because a sole proprietorship is not a legal entity, the only requirement to operate is obtaining the relevant business licenses that may apply.

Disadvantages: The owner of a sole proprietorship has full personal responsibility for the liabilities of the business. Therefore, if the business is sued, the disgruntled client can go after your home, your investments, and anything else you own. Also, certain tax planning tools available to entities are not available to sole proprietorships.

Tax Requirements: No separate tax return is required - just report profit or loss on Schedule C to your personal Form 1040. If required, make quarterly estimated tax payments. Income tax and payroll tax withholding is required if you have employees.

Sole proprietors also pay self-employment tax of 15.3% (Social Security & Medicare taxes). If you have a W-2 job, you see half this amount come out of your paycheck. Your employer pays the other half. Because a sole proprietor is self-employed, they owe the full amount. Self-employment tax is reported on Schedule SE to the Form 1040.

Legal Formation: No legal steps outside obtaining any necessary business licenses.

Unless you have no real personal assets and do not expect your business to earn more than a few thousand dollars a year, a sole proprietorship is rarely the best choice of entity.

Partnerships

If you have co-owners, the sole proprietorship is unavailable to you. Unless you actively form a different entity, the law views you as a general partnership.

Of the various kinds of partnerships, only two are really relevant here: the general partnership (GP) and the limited partnership (LP). The primary difference is that partners in a GP are jointly and severally liable for the liabilities of the business. In an LP, limited partners’ potential liability is limited to their investment in the partnership (unless they actively participate in the business). Each LP must have a general partner who technically manages the business and has personal liability. However, some basic tax planning can limit the liability of the general partner as well.

Advantages: An LP’s limited partners have limited liability. Both LPs and GPs are “pass-through” entities that do not pay income tax. Like sole proprietorships, partners report their share of partnership income or loss on their personal income tax returns. This could be advantageous if the business incurs losses that it cannot deduct immediately (due to insufficient income to offset). In that case, the losses of a GP generally can be used on the individual income tax returns of the partners to offset their other income, including investment income. Losses of an LP are often limited by the passive activity loss rules.

Another advantage of partnerships is flexibility. A partnership agreement can state how most items of income, deductions, and credits are allocated between the partners.

Disadvantages: Partners in a GP do not have limited liability. Maintaining proper books and records can quickly become very complicated with tracking capital accounts, tax basis, and specific allocations. Further, the partners are taxed on the profit or loss of the partnership, even if no cash was distributed to them. This can lead to situations where partners have tax liabilities in excess of cash to pay. Limited partners who engage in the active management of the LP may lose their limited liability protection. Again, tax planning can mitigate the loss of liability protection for active limited partners.

Tax Requirements: Although the partnership is not itself a taxable entity, it must file an annual federal Form 1065 and provide Schedules K-1 to its partners, reflecting their allocable shares of partnership income, deductions, and credits. The partners report those items on their personal returns. For withholding purposes, a partnership is treated the same as a sole proprietorship.

General partners (whether partners in a GP or serving as a general partner of an LP) pay self-employment tax of 15.3%, reported on Schedule SE of their Form 1040. Limited partners generally do not play self-employment tax unless they receive guaranteed payments from the LP.

Legal Formation: For a GP, there are no legal steps outside obtaining any necessary business licenses. For an LP, a certificate of limited partnership generally must be filed with the state in which it is formed. Although not legally required, it is highly recommended that a partnership agreement is drafted and executed. It doesn’t need to be fancy, just lay out the rights and obligations of the partners, what happens if one partner wants to sell or otherwise leave the business, how partners disputes are settled, etc.

Corporations (C Corps & S Corps)

For our purposes, there are two types of corporations: C corps and S corps. While they offer similar liability protections, they have extremely different tax treatments. The S corp is not a distinct “entity” like a C corp; rather, it is a tax election made by a C corp or limited liability company electing to be taxed as a corporation. Of the entities discussed, C corps have the most administrative burden and costs.

Advantages: The principal advantage of a corporation is limited liability. Shareholders are only at risk to the extent of their investment. They cannot be sued for corporate actions and, if the corporation is sued or insolvent, the maximum amount they can lose is the value of their investment. Also, a C corp can have different classes of stock to attract different types of investors.

S corps (like partnerships) do not pay income tax on most income (exceptions for passive income and built-in gains). S corp shareholders are allocated their proportionate share of the corporation's income, deductions, and credits (including any net operating loss deduction available). Those items are then reported by each shareholder on their respective personal tax returns. S corp owners can also benefit from reduced self-employment tax in certain circumstances using the “reasonable salary” guidelines.

Unlike limited partners, S corp shareholders can participate in the management of the entity without risk of losing limited liability.

Disadvantages: The biggest disadvantage of C corps double taxation. Corporate tax (21% in the US, plus any state tax) is paid on profits. If the corporation distributes dividends to the shareholders, the shareholders pay another level of tax. If the corporation is later sold, the sale could potentially have two levels of tax as well. As the active manager of your business, double taxation is mitigated by the requirement that the C corp pay you a “reasonable” salary. Reasonableness is determined by the market rate for the services you perform. While you are taxed on the salary, the corporation can deduct it as a business expense.

In contrast, the S corp generally is not subject to double taxation (see advantages). However, there are restrictions on S corp shareholders:

No more than 100 shareholders

Only individuals, estates, and certain trusts and exempt organizations can be shareholders

No non-resident alien shareholders

Only one class of stock (disregarding differing voting rights)

S corp shareholders are taxed on the profit or loss of the entity, even if no cash was distributed to them. This can lead to situations where shareholders have tax liabilities in excess of cash to pay.

Tax Requirements: C corps must file separate federal and state income tax returns (federal Form 1120). S corps, like partnerships, file an information return (Form 1120-S) and provide Schedules K-1 to shareholders, reflecting their allocable shares of S corp income, deductions, and credits. The shareholders report those items on their personal returns. Corporations must withhold and remit payroll and employment taxes.

To be an S corp, a valid election must be made on Form 2553 within 75 days of the start of the tax year (if you form the entity mid-year, 75 days from formation). The IRS will grant relief for late elections; however, don’t put yourself in the hands of IRS decision-makers.

If you own an S corp and operate the business, you generally must receive a salary. Any shareholder of either an S corp or a C corp who receives a salary from the entity must pay 7.65% self-employment tax. The corporation pays the other half of the tax. Amounts received in excess of salary are not subject to self-employment tax.

Legal Formation: C corps have the most setup requirements (and fees) of any of the entities discussed. They must file separate federal and state income tax returns and must withhold income and payroll taxes on wages paid. Further, a C corp must file articles of incorporation and adopt bylaws to govern its internal affairs. Most states require it to hold annual director and shareholder meetings, documented in written minutes.

S corps have no separate legal formation requirements, outside those applicable to C corps or LLCs taxed as corporations.

Limited Liability Companies

The combination of simplicity, limited liability, and tax flexibility make LLCs the most commonly-used legal entities for small business owners.

Advantages: The biggest advantages of the LLC are its simplicity and its flexibility. LLCs are limited liability for legal purposes and their tax treatment varies based on the owner(s)’ election. The owner or owners, called members, can act to have the IRS treat the LLC as a sole proprietorship (“disregarded entity”), partnership, C corp, or S corp. Therefore, many further advantages of LLCs are listed in the prior entity discussions.

Disadvantages: Disadvantages depend on which tax treatment is chosen and are listed in the prior entity discussions.

Tax Requirements: Again, the tax requirements depend upon which tax treatment is chosen. If none is chosen, the default classifications are: sole proprietorship (one owner) or partnership (two or more owners). If you want to be taxed differently, file Form 8832 indicating your election within 75 days of forming the LLC. This ensures the LLC has the desired classification from Day 1. You can later elect to tax differently in many circumstances. Once the classification is chosen, the other tax filing requirements are listed above.

Legal Formation: Generally, the filing of Articles of Organization is sufficient (one page). However, like a partnership, best practice is to draft a Membership Agreement describing the basic rights and obligations of the members.

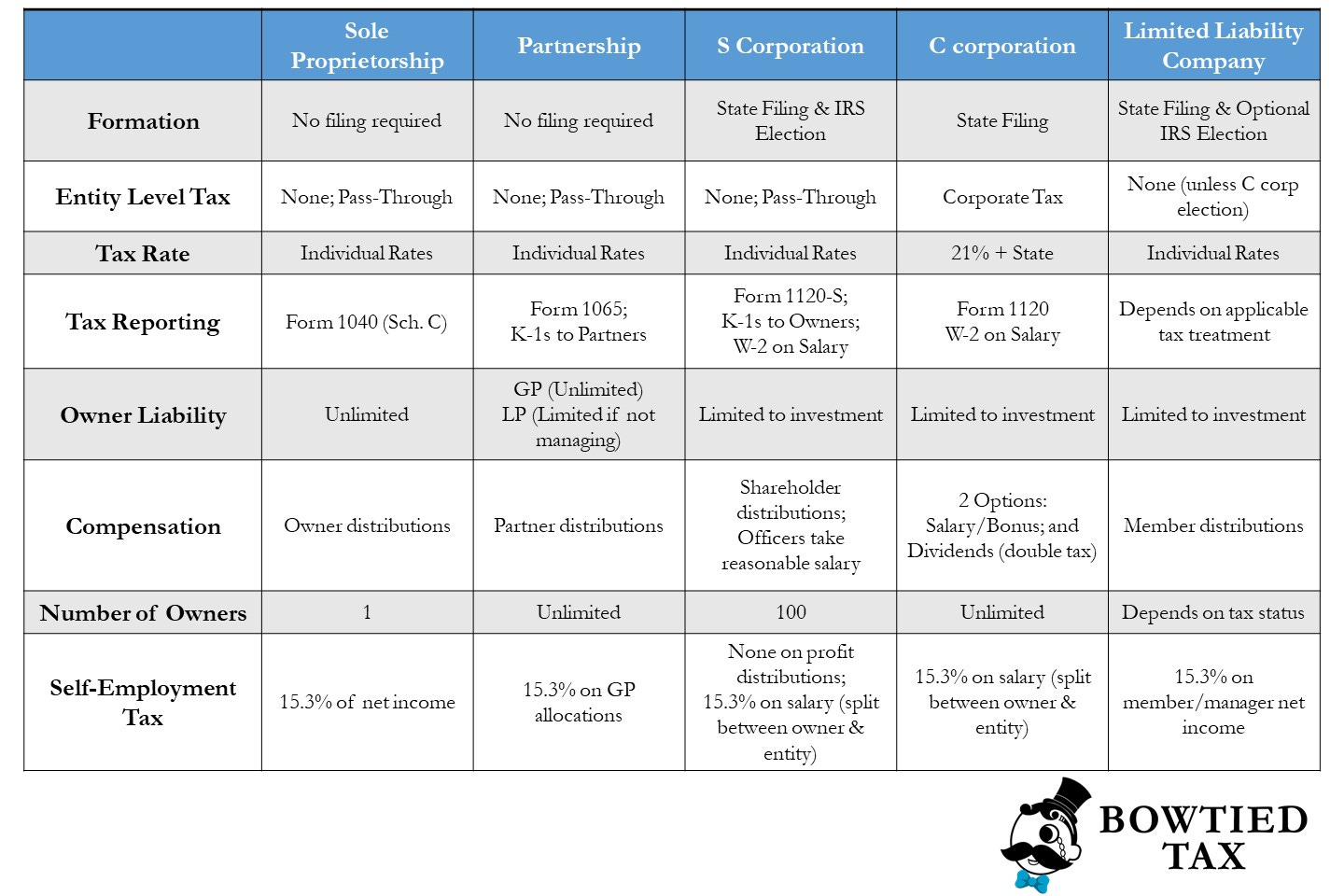

TLDR Summary: Legal Entity Quick Reference Chart

Common Deductions for Online Businesses

Because you are keeping excellent records, you know that the business is incurring a wide range of expenses. Most of these expenses are deductible.

You are allowed to deduct most expenses that are “ordinary and necessary” for business operations. Maximizing your deductions while not being overly aggressive is a pillar of good tax planning. This includes not only knowing which deductions are available, but also considering your business as a whole. Deductions should always be checked for reasonableness against your total business income. A decent tax advisor will help you achieve this.

Some of the most relevant deductions available to online businesses are listed below. Remember - there are nuances to many of these so always consult an advisor. You don’t want to get pulled into an audit because you deducted too many dinners at the neighborhood Applebee’s. But if they’re legitimate and you have detailed books and records - deduct them!

Website hosting, maintenance, internet, etc.

License fees for the tools you use (SurferSEO, Ahrefs)

Computers and other hardware used in your business (often deductible, sometimes depreciation required)

Advertising expenses

199A Qualified Business Income Deduction (up to 20% of your taxable income)

Note on 199A: Intended to benefit small businesses, this deduction can prove very beneficial to you. However, the calculation is complex and the benefit reduces at higher income levels. Talk to your advisor about your individual situation.

Employee compensation

Contractor fees (hiring developers, designers, or anyone else who is not an employee)

Half of any self-employment tax paid

Home Office Deduction (a dedicated space in your house where you primarily run your business)

Professional fees (accountants, attorneys)

Business insurance premiums

Interest paid on any business debts

Business travel expenses

Conclusion

Viewing your financial position as a whole, and armed with the information in this article, you can make an intelligent choice on structuring your business. As you operate, keep detailed records of your expenses to substantiate every deduction reasonably allowed. You’ll have more money in your pocket and fewer worries about the tax boogeyman. Now get back to making money.

If you enjoyed this article, hated it, or have any questions, reach out to me @BowTiedTrouser and visit us at bowtiedtax.com. Our email is questions@bowtiedtax.com.

Tetra here. If you have any questions for TrouserSnake feel free to ask in the comment section below.

In other news, I’ll be posting regularly on Instagram from here on out. You can follow me @bowtiedtetra_SEO (original bowtiedtetra account was banned) for regular updates.

Have you ever set up a Qualified Small Business Stock (QSBS) c-corp? Or when would you recommend it over an LLC? I see a clear advantage for a traditional startup with future sale of $20M+, but what about for something with potential to sell for $5-15M? Seems like acquirers of a biz that size usually prefer buying LLC/assets over a c-corp.